Table of Content

In this blog post, we’ll take a closer look at the difference between cash-out refinance and a home equity loan. Cash-out refinances are also generally easier to qualify for than home interest loans and offer a longer period to pay back the debt, sometimes even more than the 30 years of a typical mortgage. A cash-out refinance pays off the remaining balance on your first home loan and replaces it with a new mortgage loan. The newly refinanced loan amount is for the remaining debt owed on the first mortgage, plus the amount you’re “cashing out” from the equity. Refinance loans are generally easier to qualify for because they’re a first-lien loan.

Home equity loans, by contrast, use your equity as collateral for an entirely new loan. They are suited to individuals who need access to a reserve of cash over a period of time rather than upfront, and also come in several types. Let’s look at the differences between cash-out refinances and home equity loans so you can pick the one that’s right for you. Home-equity loans and HELOCs—or home-equity lines of credit—are similar, but not quite the same.

How much are home equity loan closing costs?

A cash-out refi replaces your existing mortgage, while a home equity loan is a second mortgage. Both refinance loans and home equity loans can put cash in a homeowner’s hands fairly quickly. In many cases, a homeowner can access the money within a few days of closing. Refinance loans are not very risky since they can take the first mortgage spot. That low-risk status often translates into lower interest rates. Home equity loans bring greater risks for lenders, so they may charge higher interest rates to account for that.

The new home equity loan will be a separate debt subject to current interest rates. In order to take advantage of these programs, borrowers need a credit score of 680 or above. Perhaps your interest rates have skyrocketed or your monthly loan payment has become more than you can afford. There is no limit on how many times you can refinance your home, but you typically have to wait at least six months between cash-out refinances. Aylea Wilkins is an editor specializing in personal and home equity loans. She has previously worked for Bankrate editing content about auto, home and life insurance.

What You’ll Be Responsible for Repaying

This may influence which products we review and write about , but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services. A home equity loan is a form of a second mortgage that allows you to borrow a specific amount without affecting your existing mortgage.

You may be required to pay a transaction fee each time you make a withdrawal or an inactivity fee if you don't use your credit line at any time during a predetermined period. During the draw period, you pay only interest on what you've borrowed. You start paying back the principal plus interest when the repayment period kicks in. Compared to rate-and-term refinancing, cash-out loans usually come withhigher interest rates and other costs, such as points.

Do You Have To Pay Taxes on a Cash-Out Refinance?

Compared to unsecured loans, such as credit cards and personal loans, home equity mortgages typically have lower interest rates, which helps keep borrowing costs low. Home equity loan interest rates are also fixed over the life of the loan, which makes it easier to budget for monthly payments. If you have sufficient equity, it’s easier to qualify for a larger sum of money with a home equity loan than other similar mortgage types. Because the cash-out is part of the new mortgage, there are no separate or unique rates charged on the funds.

During this draw period the monthly payment is usually interest-only, which allows for a more affordable monthly payment. Since mortgage interest rates are tax deductible , a home equity loan or HELOC could lower your taxable income and help you secure a larger tax refund. While you can spend that money on pretty much anything, Zillow recommends using it to improve your financial situation by paying down debt or renovating your home.

How To Flip A House And Get Started In Real Estate Investing

A home equity loan is a second loan on top of your first mortgage. Once the line of credit is approved and in place, you can withdraw money as you need it. And as you pay off the principal, you can use the credit again. We sometimes offer premium or additional placements on our website and in our marketing materials to our advertising partners. Partners may influence their position on our website, including the order in which they appear on a Top 10 list.

Recently, we’ve received quite a few calls from borrowers inquiring about home equity loans, when it was clear that what they really needed was cash-out refinancing, and vice versa. Before you choose a cash-out refinance, home equity loan, or an equity investment product, take the time to find the smartest way to access cash for your financial situation. Your best solution will depend on how much cash you need, your credit score, and your property, among other factors. A home equity loan could work if you have a strong credit score and wish to pull out a large amount of equity.

A home equity loan or home equity line of credit are mortgages that enable you to borrow against the value of your home, minus your remaining mortgage, by using your home as collateral. If you’re approved for a home equity mortgage, the lender will determine how much money you can borrow based on your home’s value and any debts against you. If you default on your home equity mortgage, the lender reserves the right to take possession of your home. If you intend to relocate within a relatively short timespan, a home equity loan might make more sense than refinancing or getting a HELOC. A cash-out refinance might have a lower interest rate, but it'll take several years to recoup the closing costs you’ll pay upfront. HELOCs also tend to have a long lifespan — 10 years for the draw period, and 20 years for repayment.

Home equity loans can be a smart choice if you still want to have a lump sum payment and can find a more competitive rate than a cash-out refinance. Or, if you’d rather have access to cash over time, a HELOC is a good choice, since you’ll have access to a draw period over a certain number of years. That way, if you have multiple repairs, home improvements, or expenses you want to pay down over time, you can withdraw from a HELOC (assuming it’s within the draw period). With a home equity loan, you receive all the money as a lump sum.

There are still plenty of times that a cash out refinance makes more sense, but it pays to do the actual analysis and look at the effects over time. But you can still see the ding on your equity from the cash out refinance. Again, the amortization factor of being further down the path with your first mortgage results in faster equity building. You can see that if you were to only look at the amount that you spend, the numbers are similar between a HELOC plus your existing mortgage and a cash out refinance. With adjustable rate products, since they are tied to a prime rate, when that rate goes up, your interest rate also goes up.

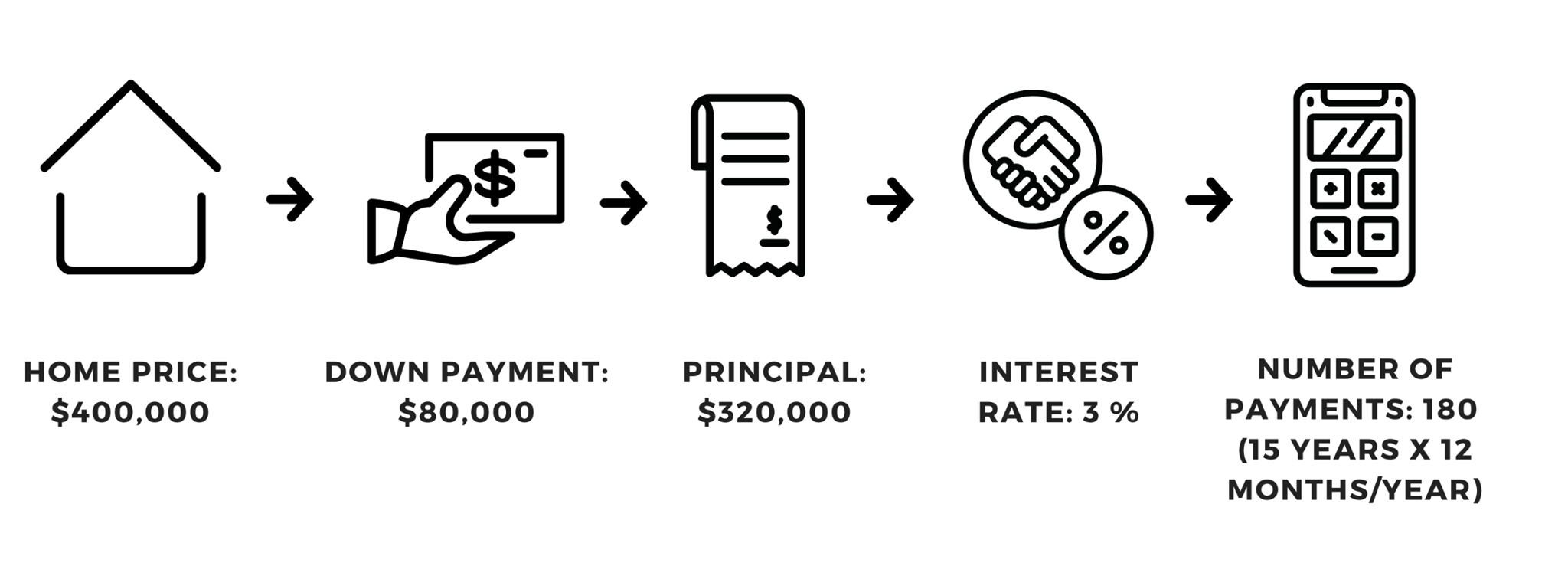

Since mortgages typically have lower interest rates than credit cards and auto loans, a cash-out refinance could save you a lot in interest over time. Generally speaking, home equity loans and HELOCs have shorter repayment terms than a primary mortgage. For example, most first mortgages are structured to be repaid over 30 years. However, home equity loans and lines of credit typically have repayment periods of 15 years or less . It is important to keep this mind because the shorter the repayment term, the higher your monthly payment will be. A home equity loan is a means of borrowing a lump sum using the equity you’ve paid into your home.

No comments:

Post a Comment